12 Min Read

You know medicine. You’ve spent years perfecting your skills, caring for patients, and running a practice that provides real value to your community. But selling a medical practice? That’s a whole different world. And if you don’t understand the financial traps lurking beneath the surface, you could be in for a wake-up call.

Think about it—how many times have you sold a business before? Probably never. Meanwhile, the buyers that are looking at your practice? Many of them do this for a living. They analyze financials, spot weaknesses, and negotiate deals designed to benefit them—not you.

Here’s where most doctors go wrong: they assume their practice will sell for what they think it’s worth. After all, you have a loyal patient base, strong referrals, and decades of dedication behind you. But when buyers start scrutinizing your numbers, none of that matters. If your financials don’t check out, your valuation crumbles.

Doctors don’t lose money on their practice sale because of clinical mistakes—they lose it because of bad financial decisions, overlooked operational gaps, poor record-keeping, unnoticed revenue declines, and bloated expenses.

If you plan to sell within the next few years (or even someday), you need to get ahead of this now. Not later. Not when you “have time.” Now.

By the time you realize you’ve made these costly financial mistakes, the damage is done. And buyers won’t care about your regrets—they’ll just move on to the next deal.

This isn’t about working harder. You’ve already done that. This is about working smarter—fixing the silent financial pitfalls that could be robbing you of the payday you deserve.

In this blog post, we’ll uncover the seven biggest financial mistakes that could be silently eating up your practice’s value—and what you need to do right now to avoid losing hundreds of thousands of dollars when it’s time to sell.

Let’s get into it.

The 7 Costly Financial Mistakes That Could Reduce Your Practice’s Value

Meet Dr. Mitchell, a renowned dentist who had built his practice from the ground up. Three decades of dedication, countless hours with patients, and a reputation that made him a respected name in his field. Now, it was time to sell.

Retirement was calling, and he was excited about the financial reward that would come from a lifetime of hard work. The offers started rolling in as well, when something shocking happened—they were far lower than he had ever expected.

Some buyers seemed interested at first but disappeared after reviewing his financials. Others used his numbers against him, picking apart his valuation, making insulting counteroffers, and questioning the long-term stability of the practice.

Dr. Mitchell was blindsided. He had expected a smooth, lucrative sale; instead, he was facing a disappointing reality—his practice was worth far less than he had imagined.

Where did he go wrong? The answer lies in seven financial mistakes that had silently drained his practice’s value. Mistakes that many doctors make without realizing the impact they can have on a sale.

1. Bloated Overhead That Sends Buyers Running

Dr. Mitchell had always believed in investing in his practice. A spacious, 5,000-square-foot office in a prime location. A large, dedicated staff that had been with him for years. The latest medical equipment, high-end furniture, and a beautifully decorated waiting area that made patients feel comfortable.

When buyers analyzed his numbers, they saw a practice drowning in overhead costs. His monthly rent alone was $15,000, nearly double the industry average for a practice of his size. His payroll expenses were eating up 55% of revenue, far higher than the standard 40%. To a buyer, this wasn’t a thriving, well-run practice—it was a financial liability.

Suddenly, Dr. Mitchell realized what was happening. While he had focused on creating the perfect environment, he had never optimized his costs. Buyers weren’t impressed by the aesthetics—they were looking at the bottom line.

Had he recognized this earlier, he could have made changes—renegotiated his lease, streamlined staff expenses, eliminated unnecessary spending—and shown buyers a practice that ran efficiently. Instead, they walked away, unwilling to take on the financial burden he had unknowingly created.

2. Declining Revenue Trends—The Silent Deal Killer

Dr. Mitchell had always assumed his practice was financially healthy. Patient volume seemed steady, and he was still bringing in good revenue. When buyers examined the numbers, they saw something Dr. Mitchell had completely missed—his revenue had been declining by 5% per year for the last three years.

The drop had been gradual, almost unnoticeable. A few long-term patients had moved away. A competitor had opened nearby, pulling in some referrals. Insurance reimbursements had been cut slightly. Individually, these seemed like small issues. Together, they were a red flag.

Downward revenue trends set off panic among buyers. They assume the practice is in trouble and things will only get worse. Long-term plans go awry and they move away from a deal.

Had Dr. Mitchell monitored his revenue trends carefully, he could have taken action—reaching out to lost patients, expanding marketing efforts, and negotiating better reimbursement rates. Instead, by the time he realized what had happened, buyers were already lowering their offers, citing “financial instability.”

3. Poor Financial Documentation—A Buyer’s Worst Nightmare

When serious buyers requested financial statements, Dr. Mitchell wasn’t ready. He had always trusted his accountant to handle the books, but now, as he scrambled to pull together tax returns, profit-and-loss statements, and balance sheets, he realized how unprepared he was.

According to a survey done by Bain and Company, almost 60% of executives attributed deal failure to poor due diligence that did not identify critical issues.

Uncategorized expenses, inconsistent financial statements, and missing documentation, all add up to a less-than-perfect due diligence, which scares investors away.

Buyers combed through his financials and instead of seeing a clean, transparent financial history, they saw risk.

One buyer even told him outright: “If your financials aren’t clear, we assume you’re hiding something.”

Dr. Mitchell wasn’t hiding anything—but that didn’t matter. Perception is everything. Buyers walked away, unwilling to take the risk of an unorganized business.

Had he worked with a financial expert years before selling, ensuring every document was pristine, this wouldn’t have happened. Instead, he was forced to watch deal after deal collapse over something that could have been easily prevented.

4. Excessive Owner Compensation That Distorts Profitability

Like many doctors, Dr. Mitchell had structured his compensation for tax advantages. He paid himself a higher salary to reduce taxable income, believing it was a smart financial move. When buyers reviewed his practice’s net income, they saw nothing but weak profitability.

According to the Economic Policy Institute, in 2022, CEOs were paid 344 times as much as a typical worker in contrast to 1965 when they were paid 21 times as much as a typical worker.

His total revenue looked great—$2.5 million annually—but after expenses, his reported profit was alarmingly low. Buyers weren’t impressed by total revenue; they cared about net income. The lower the profitability, the lower the valuation.

Had he adjusted his compensation to a market-rate salary at least two years prior, his practice would have looked significantly more profitable—and buyers would have been willing to pay more. Instead, he had to explain away the numbers, and buyers didn’t want explanations. They wanted clean, reliable data.

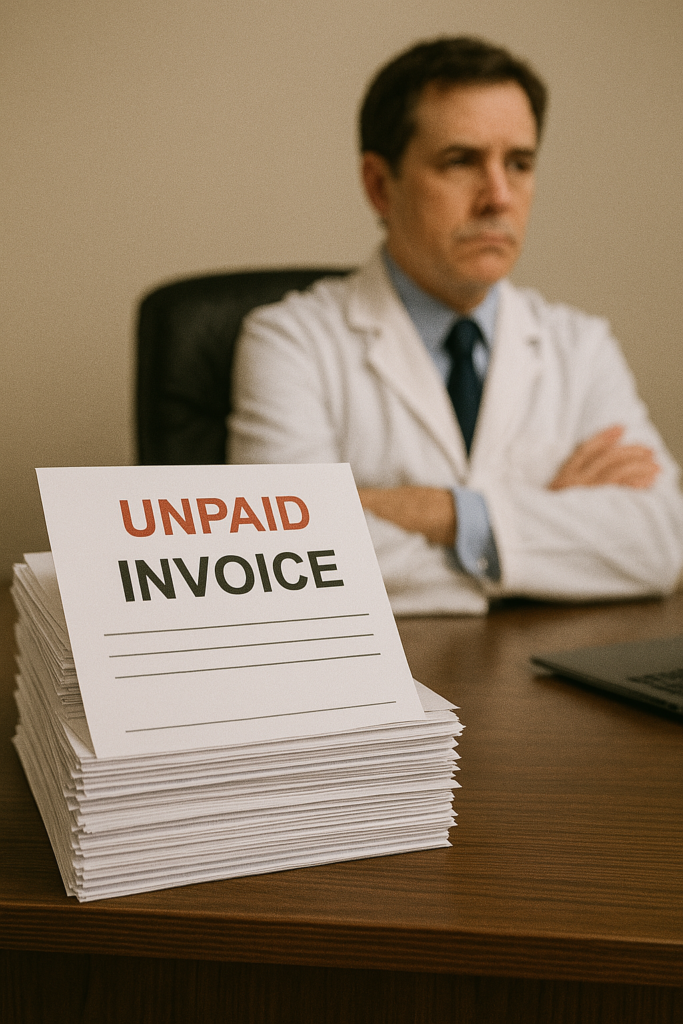

5. Uncollected Accounts Receivable—Your Hidden Pile of Lost Money

Dr. Mitchell had assumed his outstanding invoices would be the buyer’s problem. Patients owed the practice nearly $300,000, and he figured buyers would simply take over collection.

He was wrong.

Buyers saw those unpaid invoices as a financial red flag. It raised questions: Was the practice struggling to collect payments? Were patients unreliable? Was the billing process broken? Instead of seeing that money as an asset, buyers saw it as a liability—and they lowered their offers accordingly.

According to research, 70% of consumers say healthcare is the industry that makes it hardest to pay, increasing unpaid invoices.

Had Dr. Mitchell aggressively collected outstanding payments before listing his practice, he could have walked away with a much stronger offer. Instead, he was left negotiating from a position of weakness.

6. Relying Too Heavily on One Revenue Source

One of the biggest shocks for Dr. Mitchell came when buyers pointed out his revenue concentration problem. Over 60% of his income came from a single insurance contract.

At first, he didn’t see the issue. The contract had been stable for years. Yet the buyers immediately recognized the risk—what if that contract changed? What if reimbursement rates were cut? A single point of failure made his practice too risky.

According to Health Affairs, greater revenue diversification is strongly associated with higher per capita revenues.

Had he diversified his revenue sources—offering cash-pay services, broadening his insurance mix, or expanding procedures—he could have positioned his practice as a safer, more valuable investment. Instead, he had unknowingly given buyers a reason to hesitate.

7. Not Planning for Taxes—A Financial Disaster Waiting to Happen

When Dr. Mitchell finally received an offer, he was thrilled—until his accountant gave him the bad news. After taxes, he would be left with far less than he had anticipated. Nearly 35% of his sale price would be lost to taxes.

Had he worked with a tax strategist years earlier, he could have structured his sale more efficiently—using retirement accounts, tax shelters, and strategic planning to reduce his tax burden significantly. Instead, he was stuck with a massive tax bill that could have been avoided.

The Final Lesson: Don’t Let These Mistakes Cost You

Dr. Mitchell learned the hard way, but you don’t have to. These financial mistakes are preventable—but only if you take action before you sell.

Are you confident your practice will pass buyer scrutiny? If not, now is the time to fix the cracks. When buyers start looking, you want them to see a thriving, valuable practice—not a list of problems to negotiate against.

The Doctors Who Win Are the Ones Who Prepare

Imagine this: Two doctors, same specialty, similar patient volume, nearly identical revenue. One sells their practice for a life-changing sum, securing their dream retirement. The other struggles for months, watching deal after deal fall through, only to settle for a disappointing offer that barely reflects their years of work.

What made the difference? It wasn’t luck. It wasn’t just location. It was preparation. The first doctor knew that a successful sale isn’t about what a practice should be worth—it’s about what buyers see when they analyze the financials. The second doctor? They assumed everything would work itself out—until it was too late.

This is the moment that defines your financial future. Will you be the doctor who cashes in—or the one left wondering what went wrong?

Selling your practice isn’t just another business transaction—it’s one of the biggest financial moments of your life. Every dollar you lose due to financial missteps is a dollar you’ll never get back.

That’s why waiting until you’re “ready to sell” is a mistake. By then, buyers are in control, and you’re left scrambling to justify your numbers.

So, ask yourself: Are you truly prepared? Or are there hidden financial traps waiting to catch you off guard?

- Are your financials clean, clear, and ready for scrutiny?

- Have you eliminated wasteful expenses that could scare off buyers?

- Are your revenue streams stable and diversified?

- Do you have a plan to minimize your tax burden post-sale?

If you hesitated on any of these, now is the time to act. The doctors who get top dollar for their practices aren’t the ones who “hope for the best.” They’re the ones who take control of the process before buyers do.

DiligenceSure: Your Financial Safety Net

Here’s the good news—you don’t have to figure this out alone. DiligenceSure exists for one reason: to protect doctors from financial pitfalls and maximize their practice’s value.

Think of it as your pre-sale defense system. Before buyers ever see your numbers, DiligenceSure ensures they’re clean, optimized, and crystal clear. Our team of financial and valuation experts:

- Analyze your overhead and identify where buyers will see red flags

- Assess revenue trends to ensure your numbers look strong, not weak

- Clean up financial documentation so buyers don’t see disorganization or risk

- Structure your owner compensation to enhance profitability

- Ensure you collect what’s owed so you’re not leaving money on the table

- Diversify your revenue sources to eliminate financial instability

- Implement tax-saving strategies so you keep more of your hard-earned money

In short? We help you eliminate the financial mistakes that cost Dr. Mitchell—and countless other doctors—hundreds of thousands of dollars.

You’ve spent decades building your practice. Now, it’s time to get what you deserve for it. But that won’t happen if you leave your financials vulnerable to buyer scrutiny.

The difference between a disappointing sale and a life-changing one isn’t luck—it’s preparation.

So, the question is: Will you be the doctor who scrambles to fix mistakes when it’s already too late? Or will you be the doctor who takes control of your financial future right now?